KOSPI’s ~20% Drawdown vs. 6x Forward P/E: Why Technical Unwinding Creates an Asymmetric Buying Opportunity

[Key Insights at a Glance]

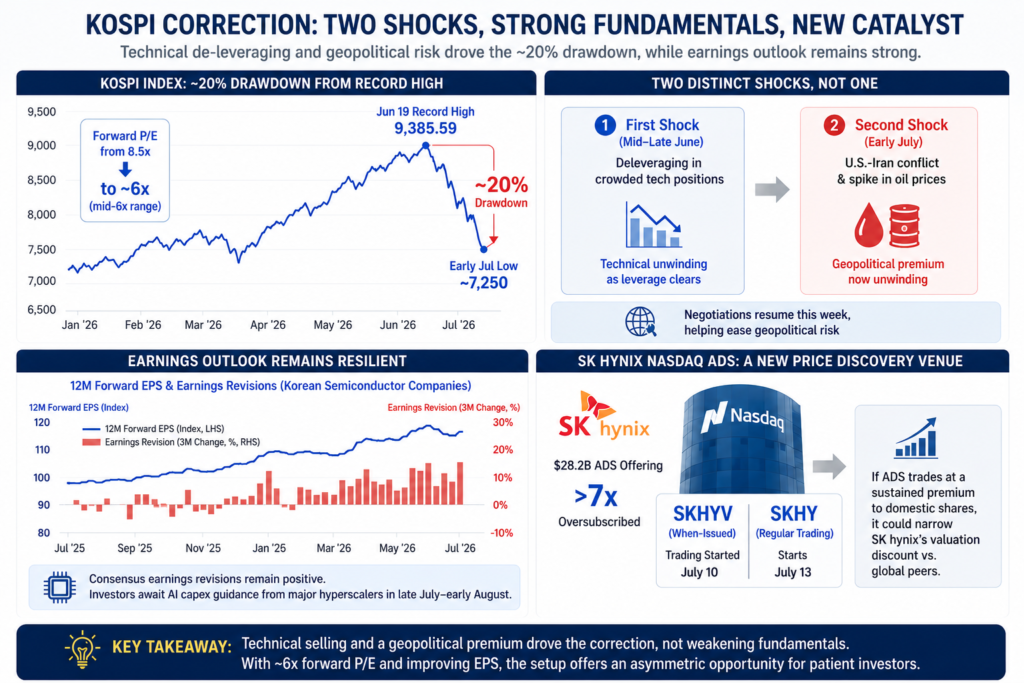

Fundamental-Price Divergence: Since its June 19 record high of 9,385.59, the KOSPI has fallen roughly 20%, while 12-month forward EPS has risen roughly 8%, compressing the market’s forward P/E from 8.5x to the mid-6x range.

Two Distinct Shocks, Not One: The June leg down reflected deleveraging in crowded tech positions; a second leg lower in early July was driven by renewed U.S.-Iran conflict and a spike in oil prices. With technical negotiations resuming this week, part of that geopolitical premium already appears to be unwinding.

SK hynix Nasdaq ADS Catalyst: SK hynix’s $28.2 billion ADS offering — reportedly oversubscribed more than 7x — began when-issued trading July 10 (“SKHYV”), with regular trading (“SKHY”) starting July 13, adding a new venue for global price discovery.

[Deep Dive Analysis]

Despite Samsung Electronics reporting preliminary Q2 operating profit of KRW 89.4 trillion, beating consensus of roughly KRW 87.3 trillion, the stock fell sharply and dragged the KOSPI lower — much of the beat had already been priced in after a strong year-to-date rally.

The correction has come in two waves. The first, in mid-to-late June, centered on crowded semiconductor positioning: after an exceptional 2025-2026 rally, elevated leverage made the market vulnerable to a sharp unwind once momentum faded. The second, in early July, coincided with renewed U.S. military action against Iran and rising oil prices, pulling the index further below its June 19 peak. This distinction matters — the first is a positioning story that resolves as leverage clears, while the second is a geopolitical premium that can compress quickly if tensions ease.

Consensus earnings revisions for Korean semiconductor names remain positive, with investors now awaiting AI capex guidance from major hyperscalers in late July and early August. Globally, the selloff has also hit crowded tech positions outside Korea — Micron, for instance, has corrected sharply despite little change in its AI demand outlook. Secular technology leaders rarely see sustained valuation declines without genuine earnings deterioration, and that fundamental deterioration hasn’t shown up here.

SK hynix’s Nasdaq listing adds a further catalyst: the 7x-plus oversubscription signals strong underlying demand for Korean memory exposure even amid the broader selloff. If the ADS trades at a sustained premium to domestic shares once regular trading begins, it could gradually narrow SK hynix’s valuation discount versus global peers.

[💡 Editor Hoi’s Insight]

The current correction reflects technical selling layered with a geopolitical risk premium — not weakening fundamentals. With the KOSPI near 6x forward earnings despite improving EPS expectations, downside risk appears limited, while the market may still be underestimating the long-term earnings power of Korea’s AI-related leaders.

Rather than marking the end of the AI investment cycle, this pullback may offer a window to build long-term positions in high-quality names. A sustained ADS premium, or further de-escalation in the Middle East, could turn the correction into an attractive accumulation opportunity. Volatility may persist until capex guidance clarifies the outlook, but today’s compressed valuations look favorable for patient investors.

Sources: Shinhan Securities, Samsung Electronics Investor Relations, Nasdaq, Yonhap News.

Disclaimer: This article is for informational purposes only and should not be construed as financial or investment advice.

Published by Inside Korea Hub