The KRW 70T Megatrend: Why SungEel HiTech is the Strategic “Pure Play” in Global Battery Recycling

[Key Insights at a Glance]

- Exponential Scalability: The global recycling market is projected to surge from KRW 22T in 2026 to KRW 70T by 2030.

- Green Premium: Proprietary hydrometallurgy slashes carbon emissions by 60-70% vs. traditional mining, meeting strict EU Battery Passport mandates.

- Non-China Supply Chain: A critical “Closed-Loop” infrastructure spanning 6 global hubs, offering a compliant solution for US IRA/FEOC regulations.

[Deep Dive Analysis]

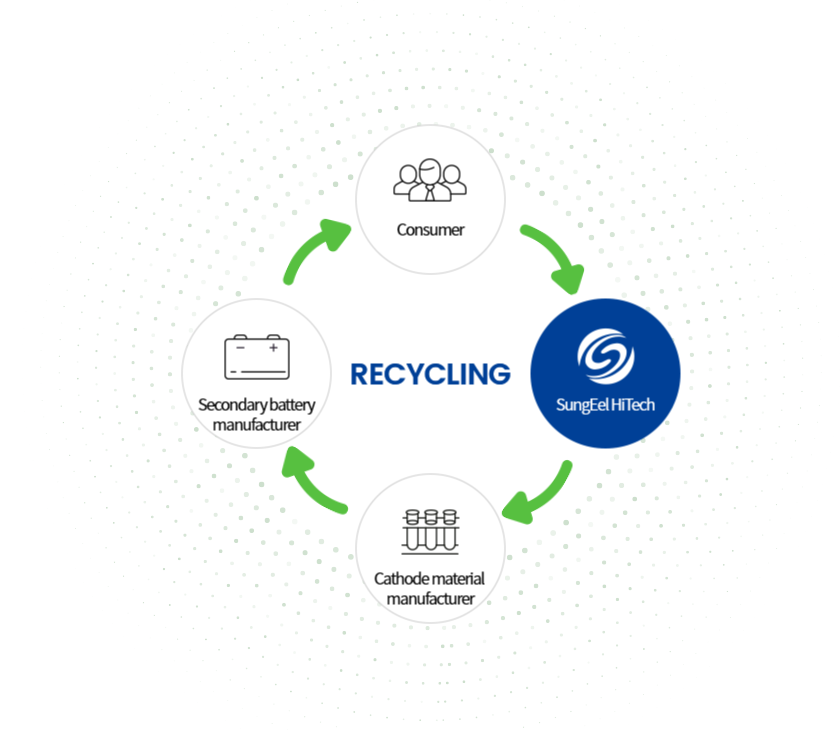

For global investors seeking structural alpha beyond cell makers, SungEel HiTech (KOSDAQ: 365340) offers a rare “pure play” opportunity. While the sector has faced a temporary “EV Chasm,” SungEel’s 2025 revenue surged 42.9% YoY to KRW 194.6B, proving its top-line resilience. The company’s competitive moat lies in its end-to-end processing capability—integrating pre-treatment with advanced hydrometallurgical extraction of high-purity Nickel, Cobalt, and Lithium.

This is no longer a tactical ESG choice but a legal mandate. With the EU’s CRMA requiring 25% recycled content by 2030, SungEel’s localized footprints in the US and Europe position it as an indispensable partner for OEMs. Despite current debt-heavy expansion, the massive influx of End-of-Life (EOL) batteries—expected to supply 68% of raw materials by 2040—guarantees a structurally secured “feedstock” that will drive long-term operating leverage.

[💡 Editor Hoi’s Strategic Insight]

We are seeing a classic valuation asymmetry. The market’s fixation on temporary margin pressure and leverage masks a guaranteed long-term trajectory. For the discerning investor, SungEel is a structural holding, not a cyclical trade. As we approach the 2026-2027 regulatory tipping point, the current price represents a strategic entry for a significant multi-year re-rating. This is the infrastructural backbone of the next EV era.

Disclaimer: Informational purposes only; not financial advice.