The 65% Profit Surge: Why EO Technics is the Unsung Hero of Samsung’s HBM4 and Nvidia’s AI Chips

[Key Insights at a Glance]

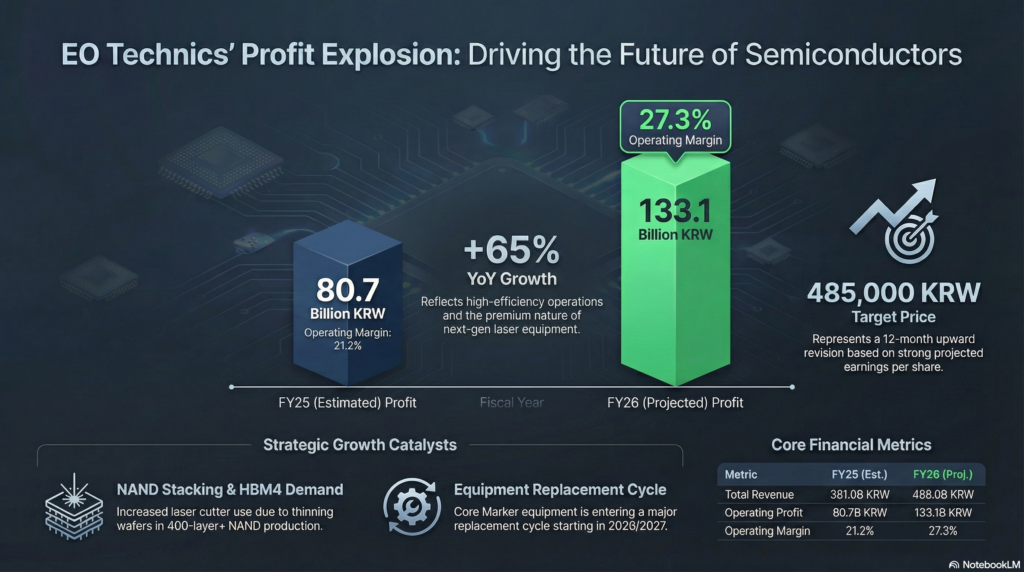

- Profit Explosion: EO Technics’ FY26 operating profit is projected to skyrocket 65% YoY to 133.1 billion KRW, with a stellar operating margin of 27.3%.

- Strategic Upgrade: Target price is set at 485,000 KRW, reflecting its monopolistic position in the next-gen investment cycle.

- Tech Shift: The transition to HBM4 and 400+ layer NAND is making EO’s laser grooving and annealing technologies an absolute necessity, not an option.

[Deep Dive: Beyond the Cyclical Noise]

EO Technics is entering a structural re-rating phase. While the market might be distracted by short-term one-off expenses (like the recent bonus payouts), the fundamental story is stronger than ever. Revenue is expected to hit 488 billion KRW in FY26, followed by a massive jump to 618.6 billion KRW in FY27.

Why now? In the AI era, chips are becoming thinner and stacks are getting higher. Traditional mechanical cutting causes chipping and heat damage. EO Technics’ specialized Laser Grooving equipment is already being deployed for its largest customer’s HBM4 lines.

Furthermore, as Samsung Electronics moves toward 1c nano DRAM (the cutting edge of memory), EO’s Laser Annealing equipment has become irreplaceable for preventing wafer warp and ensuring yield at the P4 and P5 lines. By CY26, we expect initial shipments to major US semiconductor giants, solidifying its global dominance.

[💡 Editor Hoi’s Strategic Insight]

“The recent dip due to one-off costs is a classic ‘Information Asymmetry’—a perfect tactical entry point for long-term investors. A 54.0x P/E might look expensive to some, but it is a fair price for a company that effectively holds the keys to the HBM4 and 1c nano kingdom. We are no longer betting on a cycle; we are investing in the new standard of advanced node scalability. Maintain a strong ‘Buy’.“

Disclaimer & Data Source

This analysis is based on the equity research report “EO Technics (039030): Anticipating Benefits from NAND High-Stacking” published by iM Securities on March 19, 2026.